Southern California Home Prices Hit an All-Time High

Low Supply is One Factor of Todays Soaring Market

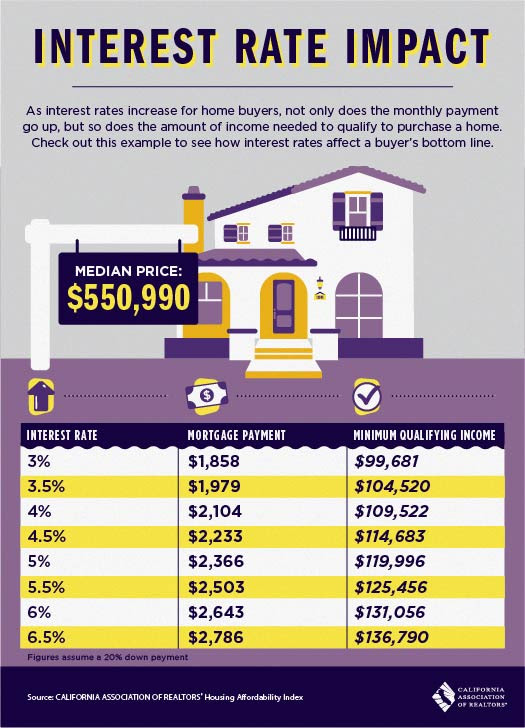

Once again, home prices are breaking records in Southern California. In April, the city's median home sale price rose 7.2 percent year-over-year and reached an all-time high of $520,000, according to a recent CoreLogic report. This data reflects a jump of $1,000 over March, according to the Los Angeles Times who first broke the news. The median price for new and resale houses and condominiums in Los Angeles County spiked 7.3 percent to $590,000. Prices rose between 4.4 percent and 10 percent for the other five counties in the SoCal region.

However, sales activity was down 1.5 percent in comparisson to last year. This is likely because of low inventory and prices rising beyond what many buyers can afford or are comfortable shelling out. According to Freddie Mac, average interest rates on a 30 year mortgage also jumped to a seven year high of 4.61 last week.

These Southern California trends mirror both the state of California, and the nation. California's median sale price has risen for 73 consecutive months since March 2012, according to CoreLogic. National home sales are strong as well, especially sales above the $750,000 mark, tempered only by a low supply of homes, according to the National Association of Realtors.

There are signs that younger buyers could continue to drive demand. According to the LA Times, first-time buyers made up 38 percent of single-family home purchases last year, the highest percentage since 2000.

In a real estate transaction it is not uncommon for the seller to wish to remain in the property for some period of time after the close of escrow. One potential reason for this could be that the seller is moving and needs more time to prepare, or to solidify the deal on their next home. This situation became frequent enough that the California Association of Realtors® (C.A.R.) produced a contract called the Seller License to Remain in Possession Addendum. This C.A.R. form, often reffered to as the SIP, is intended for a short-term occupancy after the close of escrow. In this case, short-term occupancy is considered thirty days or less. If a seller should require a longer period of time, C.A.R. has a more detailed agreement called the Residential Lease After Sale, often reffered to as a seller leaseback.

The short-term occupancy agreement, or SIP, allows the seller to specify their occupancy terms as either number of calendar days after close of escrow, or up until a specific date. The consideration section of the agreement indicates the amount to be charged for the given time period whether in the form of cost per day or total cost. It also accounts for a late fee if a payment following the close of escrow is overdue. In addition, this contract covers who shall pay for utilities and maintenance, states that the buyer shall be allowed entry for a variety of reasons with the required 24 hours notice, instructs that the seller shall not assign or sublet any part of the property, and advises the seller to obtain insurance for personal property during this period.

Navigating through the labyrinth of details and information of a transaction is exactly why you, savvy buyers and sellers, need an experienced team. The SARKISSIAN + PERERA GROUP is here to help guide you through this process and ensure that you achieve all of your real estate goals!

Berkshire Hathaway HomeServices California Properties • 11828 Rancho Bernardo Road Suite 210

San Diego, CA 92128 (858) 792-6085 • http://www.bhhscal.com