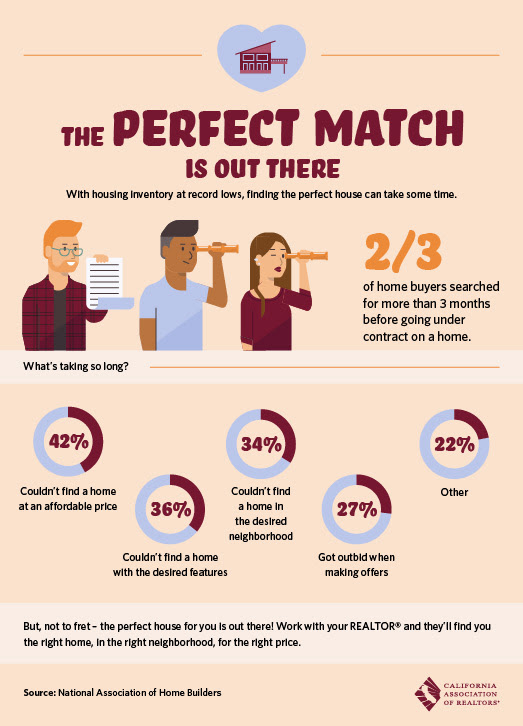

Spring Home Sales

The coming months will be a true test of the housing market. Rising mortgage rates, the new tax bill, and weariness of first-time buyers are all expected to reduce demand. Spring home sales could be the weakest we’ve seen in years.

The economy is on the rise, pay rates are increasing, and millennials are creating families. Despite these home-purchasing factors, some real estate agents feel this could be one of the weakest spring seasons in years. The potential reasons for this are: mortgage rates are on the rise, the new tax law reduces homeownership incentives, and first-time buyers are increasingly nervous about being excluded from the competitive market. The outcome of this is expected to be reduced demand for homes this year. The next few months will be a crucial test of the market. Approximately 40% of the years’ sales occur between March and June, according to the National Association of Realtors, because buyers are eager to close the deal before summer vacation and the start of the upcoming school year.

It is possible that the outrageous price increases of the past years will level off due to sales volumes that are expected to be underwhelming. This situation provides an opportunity for savvy buyers willing to brave the market and higher interest rates, but also challenges sellers in upscale markets. Daren Blomquist, a senior vice president at the housing-research firm of Attom Data Solutions states “It’s still going to be a tight market, but we’re moving from an extremely tight market to one that has some wiggle room around the edges for buyers”.

Chief Economist of the National Association of Realtors, Lawrence Yun, said that he expects sales to be flat this spring compared to a year earlier. Almost 2.1 million homes were sold between the months of March and June in 2017, an increase from approximately 2 million from the same quarter in the previous year, according to the National Association of Realtors. Yun has also predicted that sales will remain stagnant throughout 2018 due to a lack of inventory and unaffordability with prices and mortgage rates escalating.

Nationally, pending home sales, an indicator of upcoming activity, dropped 4.7% in January to the lowest it has been in over 3 years. According to the National Association of Realtors, existing home sales decreased in this same period of time by 4.8%. Meanwhile, the median price rose 5.8% from the prior year, making it the 71st straight month of annual gains. Fannie Mae released statistics that indicated consumer confidence in the housing market had fallen by 5% due to concerns regarding stock market instability and increasing mortgage rates.

The top end of the market is slowing across the country, partly due to the tax overhaul, which capped both mortgage-interest deduction and state & local tax deductions, disproportionately affecting higher-priced homes. On the opposite end of the market, rising interest rates are essentially pricing buyers out. California is also experiencing a decrease, January sales dropped 7.6% since December and were 2.9% lower than the same month a year ago, according to the California Assocation of Realtors.

Some realtors have reported heightened activity in the past weeks, signaling an understanding of and adjustment for the new tax law. Buyers are making larger down payments in order to bring their mortgages below the new $750,000 cap. In addition, older buyers are considering selling their homes and utilizing those earnings for out of state retirement. Both of these elements are expected to increase inventory in the coming months. |