:format(webp)/cdn.vox-cdn.com/uploads/chorus_image/image/58058663/GettyImages_470165439__1_.0.jpg)

Republicans say the Tax Cuts and Jobs Act is a massive tax cut that will spur investment, jobs, and economic growth. But Democrats counter that the bill is a brazen effort to loot the American government, with an eye toward unraveling social safety programs like Medicare, Medicaid, and Social Security.

But having passed the House and Senate, the bill is now a President Trump signature away from becoming the law of the land, so what does it mean for you, the taxpayer?

In the past, tax reform efforts have tried to simplify the tax code and remove special-interest deductions that have become entrenched since the United States ratified the income tax in 1913. The Tax Cuts and Jobs Act makes no attempt to simplify the code; if anything, it does the opposite, introducing new loopholes while making only a minor effort to reel in special interests.

The bill’s primary function is a massive corporate tax cut, dropping the rate from 35 percent to 21 percent. Individuals will get an across-the-board cut as well, albeit small, but in an attempt to offset some of the $1.5 trillion cost, the individual cuts expire after 2025.

How does this impact you? We’ll walk you through the basics:

Individual rates fall, standard deduction doubles

The good news is that in 2018, you’re probably getting a tax cut. The individual rates fall across the board. The new law not only lowers rates across all seven tax brackets, but lowers the threshold for each bracket. This applies to taxpayers who file jointly as well.

The new law also doubles the standard deduction to $12,000 for individuals and $24,000 for joint filers. For taxpayers with few itemized deductions, this means taking the standard deduction will exempt twice as much of your income from federal taxation. For those who currently itemize, it may now make sense to simply take the standard deduction, and thus have less income subject to federal taxation as well.

Below, you can adjust the slider at the bottom to match your income to see how the law changes for you. If you file jointly, click the right arrow at the bottom of the visual to see how your circumstances change.

But the benefits to the poor and middle class are temporary

While the corporate tax cut is permanent, the majority of the individual cuts expire on December 31, 2025, setting up yet another potential “fiscal cliff.” Republicans have said they intend and expect to extend these tax breaks when the time comes.

But under the law as it stands, they expire, and that’s led a number of nonpartisan analyses to conclude that while the poor and middle class get a tax cut in the short-term, most of the long-term benefit is to the rich.

While supporters of the bill say the corporate tax cut will lead to more investment, more jobs, and higher wages, there will undoubtedly be a windfall to corporate shareholders as companies kick their tax cuts back to investors in the form of dividends. But as only 45 percent of Americans own stock, and only 14 percent own stocks outside of a 401(k), this benefits mostly the rich.

:format(webp):no_upscale()/cdn.vox-cdn.com/uploads/chorus_asset/file/9899719/tpc1.png)

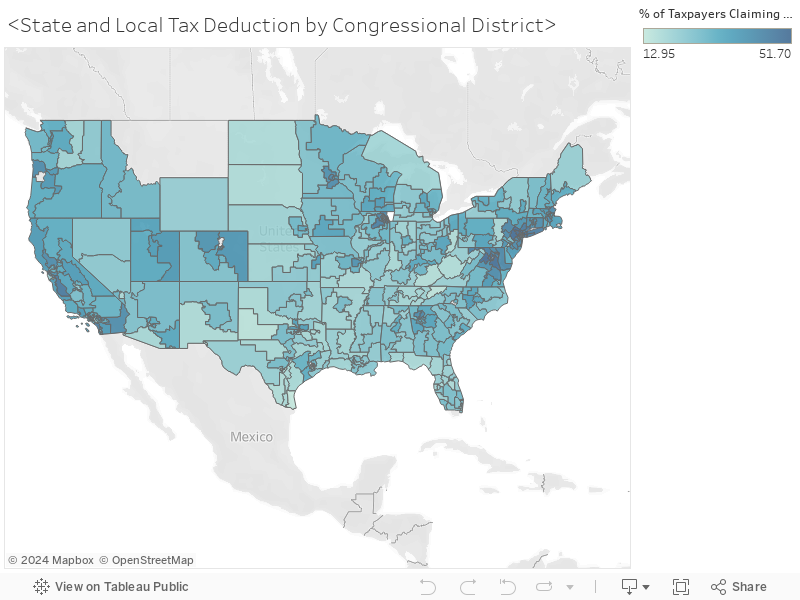

State and local tax deductions are capped at $10,000

Currently, taxpayers can deduct what they pay in state and local property, income, and sales taxes from their federal returns. The new law caps these deductions—which can be any combination of property, income, and sales taxes—at $10,000.

If you live in a coastal city with high local and state taxes—and particularly if you own a home on which you pay property taxes—this could have a huge impact on your final tax bill, even with the lower rates and doubled standard deduction.

Of course, high-tax states and cities tend to be on the coasts—and tend to vote Democratic. Republicans have been accused of attacking blue states with this measure, and the 12 Republicans who voted against the bill in the House largely did so on the basis of the cap on SALT deductions.

Below, you can see how often SALT deductions are claimed in your area to see if this will impact you. If you’re using Google Amp, you may have to open the full page to see it.

The cap on mortgage-interest deduction drops to $750,000

The real estate lobby is one of the most powerful and active on matters related to the tax code, and the mortgage-interest deduction has long been considered a sacrosanct pathway to the American dream of owning a home. That’s why even though the cap is higher than the $500,000 the House proposed, it’s surprising that it was changed at all.

Because most people’s home values don’t exceed $750,000, this is another measure that affects mostly coastal blue-state cities with expensive housing markets, and it only applies to new mortgages. The National Low Income Housing Coalition estimates that just 1.9 percent of mortgage originations from 2013 to 2015 exceeded $750,000 in value; California accounted for 45.7 percent of them, and New York accounted for 7.4 percent.

The new cap won’t apply to existing mortgages, just new ones. And because of the doubled standard deduction, this may not affect you if you forgo itemizing. A Zillow study estimated that roughly 44 percent of U.S. homes are worth enough for it to make sense for a homeowner to itemize and take the MID under current law. Taking into account the new standard deduction, SALT changes, and MID cap into account, that number drops to 14.4 percent under the new law.

That’s bad news for the real estate lobby and wealthy property owners, as Moody’s Analytics estimates that home prices will drop 4 percent nationwide compared to projections without the new tax law.